This is a series called micro project that I am going to share part of my projects.

Last year I did my undergraduate paper in high-frequency votaility modeling with 5 minute data collected from US stock market. Now I decided to make some improvements.

The main approach is Lasso regression for single asset, and Cholesky decomposition applied for multi assets. For short, I will just show plots and results rather than the model itself.

Data

I employ 5 minute data from crypto coins.

| BTC | ETH | SOL | XRP | |——|——-|——|——|

The stocks are choosen on personal preference, since there’s no any requirement.

Time period is from 2023-12-01 to 2025-11-01, since I get data from massive this time, the free account only can access to last two years.

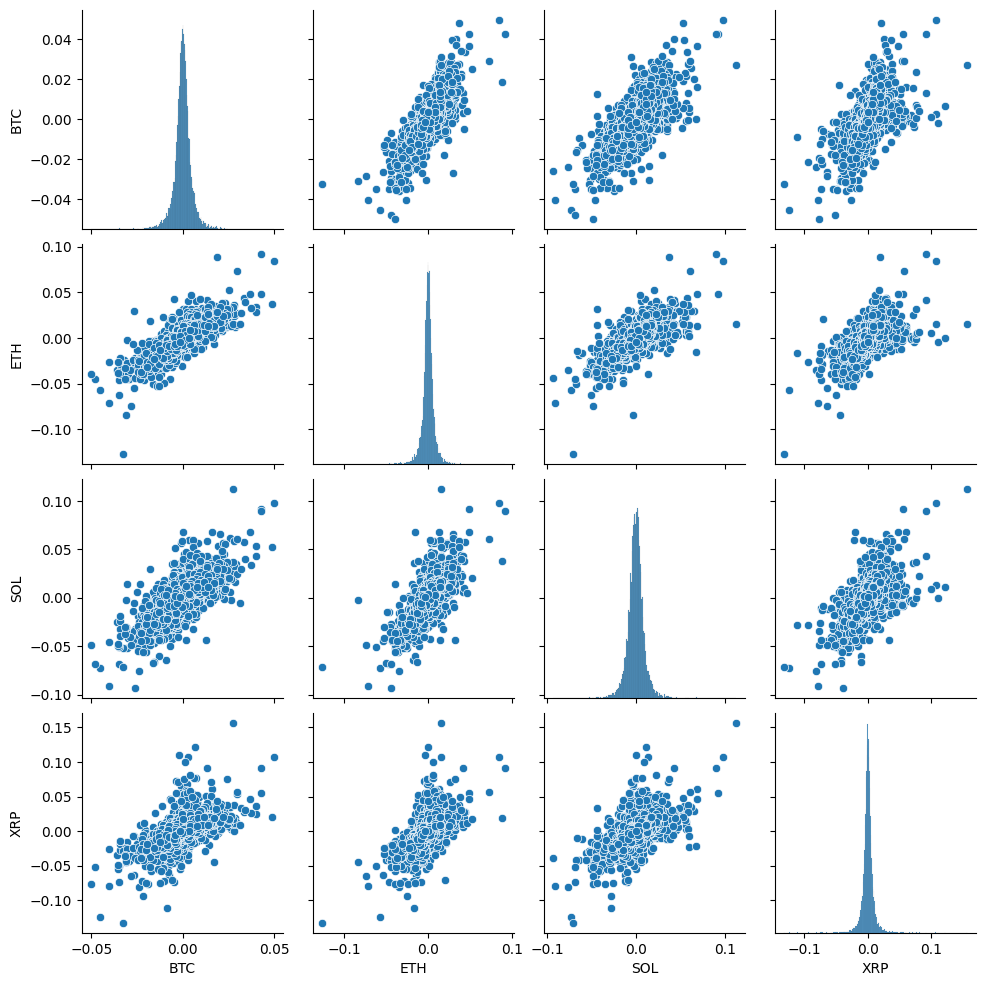

From the joint plot of log return of crypto currencies, there’s most significant linear correlation between BTC and ETH.

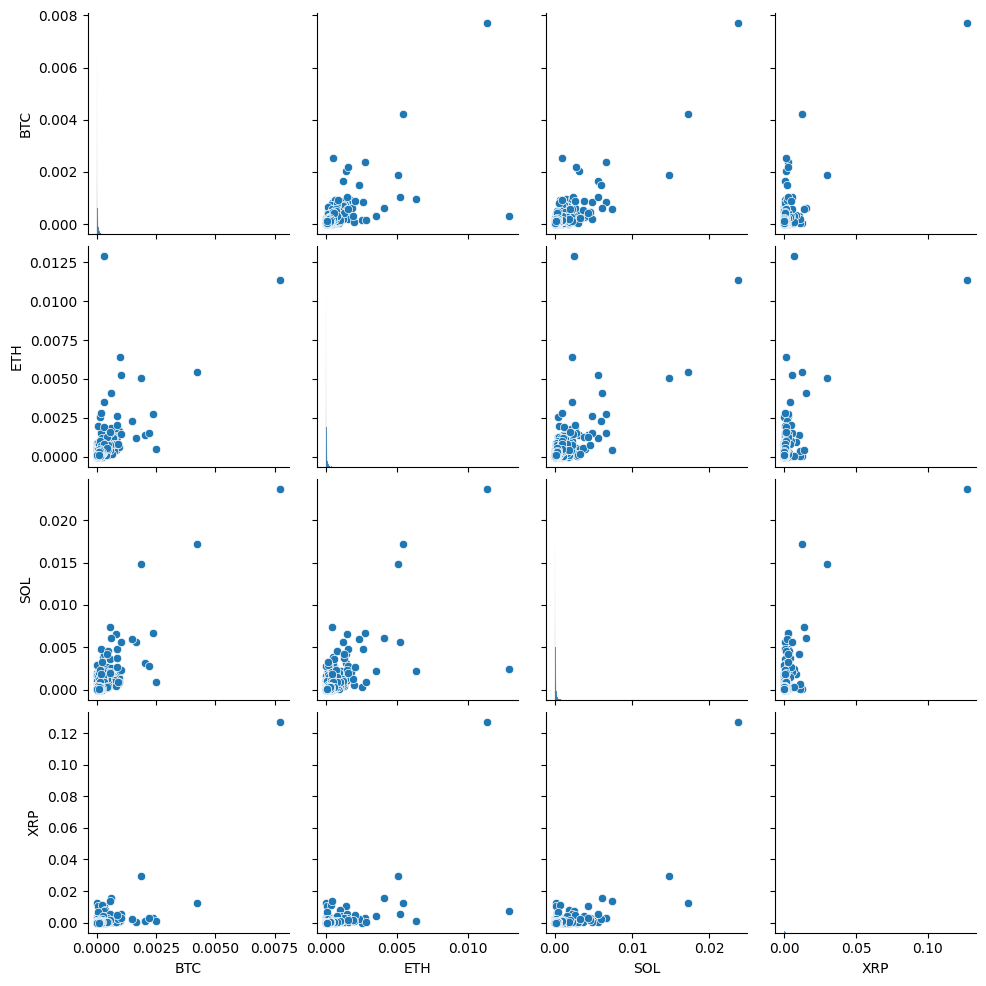

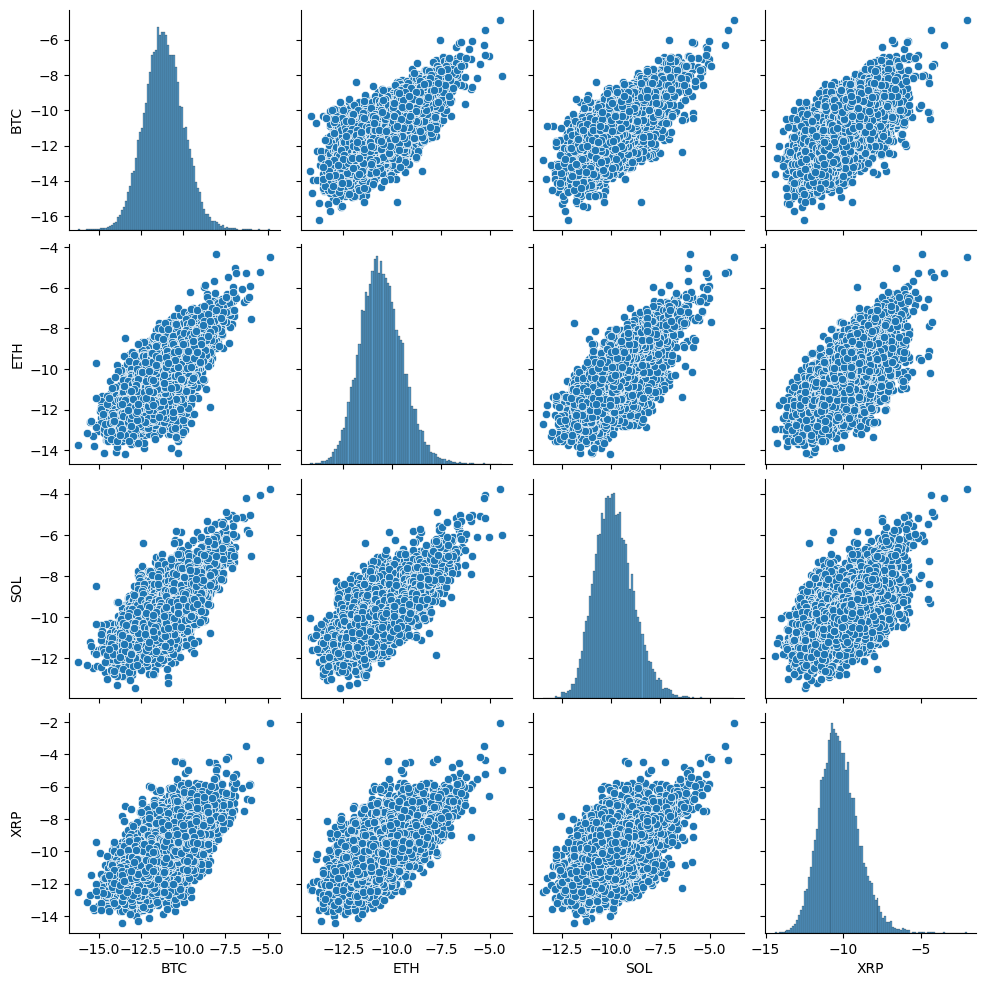

The plot of RV is terrible, but after log-transformation, although the correlation coeffective doesn’t change alot, looks more normal.

Model

I will use Lasso regression, Group Lasso, Sparse Group Lasso, and LSTM model.

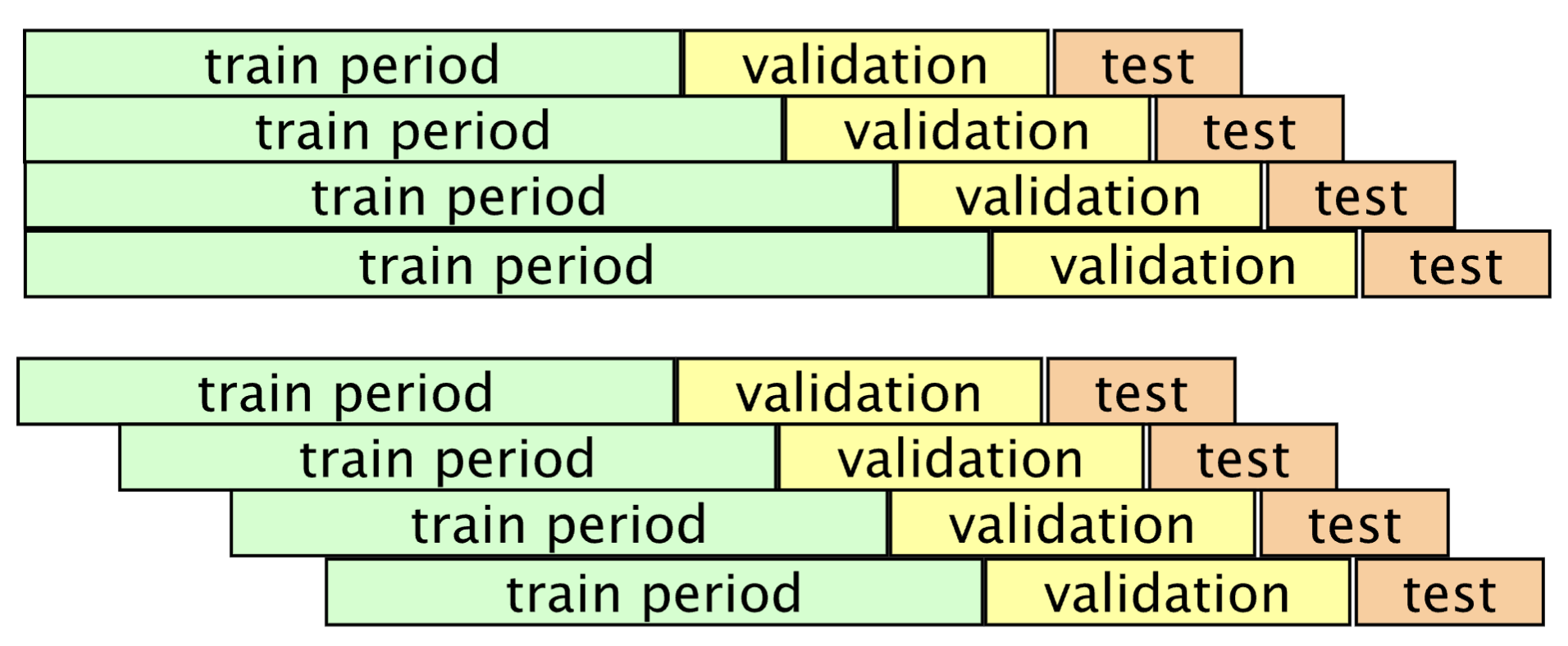

There’re also two ways to move the sample: increasing train period or just keep fixed size.

Result

TODO

-

Previous

Algo Note: the idea of some sorting algorithms -

Next

LeetCode 2435 | Simple Steps: Write a Simple DP and a Space Optimized DP